The Fundamentals of Real Estate and Property Protection

Owning real estate is a significant achievement for many of us, whether it’s our personal home or an investment property. Yet, in May 2026’s intricate housing market, these valuable assets face increasing threats. Think of unexpected lawsuits, creditor claims, and sophisticated fraud schemes.

With over 100 million lawsuits filed in U.S. state courts each year, the need for strong real estate and property protection strategies is more critical than ever. We believe proactive planning is essential to preserving our wealth.

This extensive guide will empower us with the knowledge to shield our real estate from potential financial ruin. We will define real estate asset protection and explain its vital importance. We’ll also explore common risks like liability claims and fraud.

Our focus will be on effective strategies, including the smart use of LLCs, trusts, insurance, and even equity stripping. Understanding your property’s value and vulnerabilities is key; for valuable insights into your home equity, we often recommend exploring home equity insights. We aim to provide a clear roadmap for combining these protective measures with tax and estate planning, ensuring our real estate investments remain secure.

The landscape of real estate ownership is fraught with potential pitfalls, from the ever-present threat of lawsuits to the challenges posed by creditors and unforeseen financial liabilities. Protecting our real estate assets isn’t merely about safeguarding physical structures; it’s about preserving our financial well-being and ensuring the longevity of our investments. The sheer volume of legal actions in the U.S. underscores the necessity of a robust defense strategy.

Defining Asset Protection for Property Owners

Real estate asset protection is a strategic framework designed to shield a property owner’s assets from potential legal claims, creditors, and other financial threats. It’s about establishing legal barriers that prevent personal wealth from being seized to satisfy judgments or debts related to our real estate holdings. Without proper protection, a single lawsuit or an unpaid debt could lead to the forced liquidation of valuable properties, jeopardizing our personal finances and future investment opportunities. The goal is to create a secure environment where our assets are less vulnerable, ensuring that our hard-earned equity remains intact. This proactive approach helps us maintain control over our investments, rather than having them dictated by external legal or financial pressures.

Why Proactive Planning is Essential in May 2026

In May 2026, the need for proactive asset protection planning is more pronounced than ever. The statistic that over 100 million lawsuits are filed in U.S. state courts annually highlights a pervasive legal risk environment. These lawsuits can range from personal injury claims stemming from incidents on our property to disputes with contractors or tenants. Without a pre-established protection plan, our real estate assets can become direct targets, potentially leading to significant financial losses.

The legal system often operates on the principle of “deep pockets,” meaning those with substantial assets are frequently pursued more aggressively. Waiting until a lawsuit is filed or a creditor comes knocking is often too late, as many protective measures can be challenged or deemed fraudulent if implemented after a claim arises. Therefore, establishing a comprehensive asset protection plan before acquiring properties or before any legal issues surface is paramount. This foresight allows us to structure our ownership in a way that minimizes exposure and maximizes financial shielding against unexpected judgments.

Feature Primary Residence Protection Investment Property Protection Primary GoalPreserve home equity, maintain residency Limit liability, maximize returns, ensure privacy Key StrategiesHomestead exemption, robust homeowners insurance, living trusts LLCs (single or Series), anonymous trusts, landlord insurance, equity stripping Liability Exposure Generally lower, but still vulnerable to personal injury claims Higher due to tenant interactions, visitor traffic, property conditions Insurance Needs Standard homeowners insurance, umbrella policy Landlord insurance (liability, loss of income), umbrella policy Privacy ConcernsLess critical, but trusts can offer estate planning benefits High, especially for high-net-worth individuals or large portfolios Tax Implications Mortgage interest deduction, capital gains exclusion Depreciation, operating expenses, potential self-employment tax Legal Structures Personal ownership, revocable living trust LLCs (single or Series), land trusts, anonymous trusts Structural Strategies for Asset Shielding

Building a resilient real estate portfolio requires more than just acquiring properties; it demands a strategic approach to ownership structures that can shield assets from potential threats. Legal entities like Limited Liability Companies (LLCs) and various forms of trusts are foundational tools in this endeavor. For those managing multiple rental units, especially in vibrant markets like Detroit, understanding how to structure ownership effectively can significantly reduce personal exposure. Explore options for managing a Detroit furnished property, for example, to see how different ownership models might apply.

Utilizing LLCs for Real Estate and Property Protection

Limited Liability Companies (LLCs) are a cornerstone of real estate asset protection, offering a crucial layer of separation between our personal assets and our business liabilities. When we own real estate through an LLC, the company, not us personally, is typically responsible for debts and legal obligations related to that property. This means that if a tenant is injured on the property and sues, or if a contractor files a lien, the lawsuit generally targets the LLC’s assets, not our personal bank accounts, primary residence, or other investments. This compartmentalization is invaluable for preventing a single adverse event from jeopardizing our entire financial standing.

For investors with multiple properties, a Series LLC can offer an even more efficient structure. A Series LLC allows us to create multiple “series” or “cells” within a single master LLC, with each series acting as a distinct legal entity. This means each property can be held in its own series, isolating its liabilities from other properties in our portfolio. If one property faces a lawsuit, only the assets within that specific series are at risk, preventing cross-liability that could otherwise affect our entire portfolio. This approach is particularly beneficial for those managing diverse real estate holdings, such as various types of residential properties, including unique options like Alameda short sale townhouses. By understanding and implementing these business entities correctly, we can significantly bolster our personal liability protection.

The Role of Real Estate Trusts and Shell Companies

Beyond LLCs, real estate trusts and, in some contexts, shell companies, play a significant role in enhancing asset protection and privacy. Anonymous trusts, often structured as land trusts, are particularly effective for maintaining privacy of ownership. With a land trust, the trustee’s name appears on public records as the owner, while our identity as the beneficiary remains undisclosed. This anonymity can be a powerful deterrent against frivolous lawsuits, as potential plaintiffs may find it difficult to identify the true owner and assess their net worth. The beneficiary still retains control over the property, including the right to sell, lease, or mortgage it, but without public exposure.

While the term “shell company” can sometimes carry negative connotations, in the context of legitimate asset protection, it refers to legal entities established primarily to hold assets and provide layers of separation. These can be various types of LLCs or corporations, sometimes domiciled in states with strong privacy laws. When combined with trusts, these structures can create a multi-layered defense that makes it exceedingly difficult for creditors or litigants to penetrate. For instance, holding properties like Cromwell foreclosed condos within such a structure can add an extra layer of privacy and protection, shielding the beneficial owner from direct public scrutiny. The strategic use of these entities is about creating legal distance and obscurity, making our assets less attractive targets.

Defending Against Modern Fraud and Liability Risks

The digital age has introduced new complexities to property ownership, making modern fraud and liability risks more sophisticated than ever. From deed fraud to title theft, property owners must be vigilant and employ advanced defense mechanisms.

Combating Deed and Title Fraud

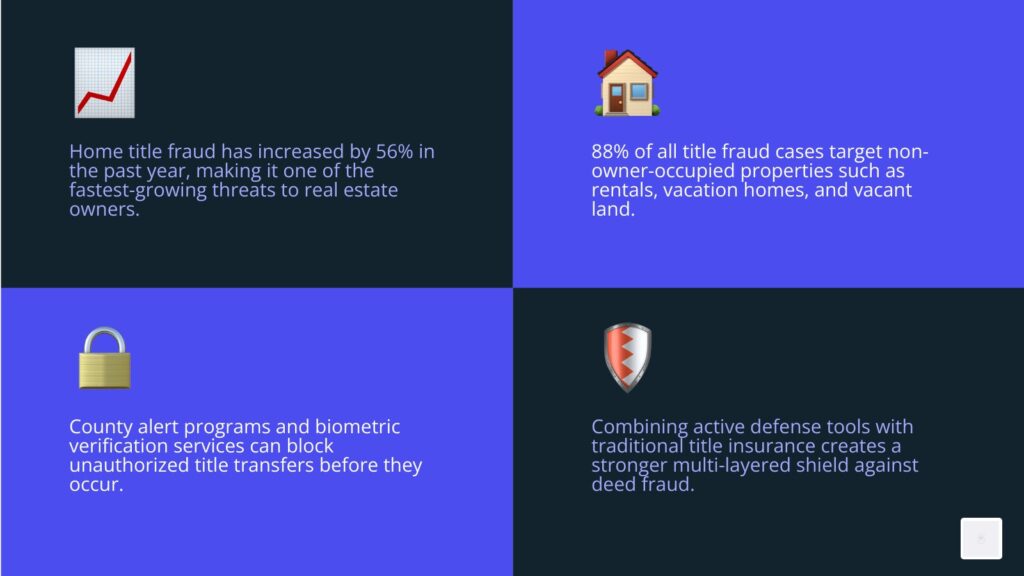

Deed fraud and title fraud represent insidious threats that can strip us of our property without our knowledge. These schemes often involve criminals forging documents or impersonating owners to illegally transfer property titles. A particularly alarming trend in May 2026 is the significant increase in home title fraud, which surged by 56% in the past year. This type of fraud disproportionately targets non-owner-occupied properties, such as rental units, vacation homes, and vacant land, with a staggering 88% of cases falling into this category. Only 12% of title fraud cases involve owner-occupied homes, highlighting the heightened vulnerability of investment properties.

To combat this, a multi-pronged approach is essential. Beyond traditional title insurance, property owners should consider proactive measures such as registering for county property alert programs, which notify us of any recorded documents affecting our property. Services offering “active defense” can go further by recording a public notice on the property, effectively “locking” the title and requiring owner biometric verification for any transaction. This creates a legal barrier that blocks unauthorized transfers before they occur. For those with diverse real estate portfolios, including properties like Washtenaw County foreclosed houses, staying informed and utilizing these advanced protection mechanisms is crucial to safeguard against these modern threats.

Insurance as a Critical Safety Net

While legal structures form the backbone of asset protection, insurance acts as a vital safety net, covering risks that legal entities alone cannot. For real estate investors, landlord insurance is indispensable. This specialized policy typically covers property damage, liability for injuries sustained on the premises by tenants or visitors, and even loss of rental income if the property becomes uninhabitable. It’s crucial to understand the limitations, however; insurance providers may refuse to cover instances of gross negligence or certain large judgments. Therefore, while a powerful tool, it’s not a standalone solution.

For owner-occupied homes, comprehensive homeowners insurance is the standard, covering dwelling, personal property, liability, and additional living expenses. For both types of properties, an umbrella liability policy can provide an extra layer of protection, extending coverage beyond the limits of standard policies. When dealing with title-related risks, standard title insurance is a one-time purchase at closing that protects against issues existing before the purchase. However, it often has limitations regarding post-closing fraud, especially for properties held in business entities. Enhanced policies, like certain ALTA (American Land Title Association) forms, might offer broader coverage but often exclude properties held by LLCs. This gap underscores the need for additional layers of protection. For comprehensive property protection, it’s wise to consult with providers who understand the nuances of real estate risks and can offer tailored solutions, such as those specializing in Stanton property protection.

Advanced Financial Tactics and Privacy Measures

Beyond legal structures and insurance, sophisticated financial tactics and privacy measures can significantly enhance real estate asset protection. These strategies are designed to make our properties less attractive targets for lawsuits and to obscure our ownership from public scrutiny. Understanding our home equity insights is a critical first step in implementing these advanced tactics.

Equity Stripping for Real Estate and Property Protection

Equity stripping is a strategic financial maneuver designed to reduce the apparent equity in a property, making it a less appealing target for potential litigants or creditors. The principle is simple: if a property has little to no accessible equity, it offers limited financial incentive for a lawsuit. This strategy often involves recording mortgages or liens against the property’s equity, typically through loans from friendly parties or other controlled entities.

A common approach is to maintain a high loan-to-value (LTV) ratio, often around 75%. This means that 75% of the property’s value is encumbered by debt, leaving only 25% as accessible equity. In the event of a lawsuit, a plaintiff might look at the property’s encumbered status and decide that the cost and effort of pursuing a judgment against a property with limited accessible equity outweigh the potential recovery. This tactic has been upheld in various legal precedents, where recorded mortgages have protected property equity from judgment liens. While the concept of offshore trusts is sometimes associated with more complex equity stripping strategies, the core idea revolves around creating legitimate debt against the property. This can be particularly relevant for investment properties, including commercial foreclosures in areas like North Port, where minimizing visible equity can be a strategic advantage.

Maintaining Anonymity in Public Records

For many real estate investors, privacy is a paramount concern. Maintaining anonymity in public records can deter potential litigants, protect against targeted fraud, and simply offer peace of mind. This is where strategies involving nominee trustees and sophisticated trust structures become invaluable.

When we purchase property, our name typically appears on the deed in public records. However, by utilizing a land trust with a nominee trustee, the trustee’s name is recorded as the legal owner, while our identity as the beneficial owner remains confidential. This means that anyone searching public records will only find the trustee’s name, not ours. This layer of separation can be critical in preventing our personal wealth from being linked directly to our real estate holdings.

Similarly, shell companies, when properly structured and used legitimately, can also serve to conceal ownership. For instance, a property might be owned by an LLC, which in turn is owned by a trust, which then has an anonymous beneficiary. This multi-layered approach creates significant hurdles for anyone attempting to uncover the ultimate beneficial owner. This level of identity concealment is a proactive measure that can reduce our exposure to various risks. For those investing in new construction houses in developing areas, establishing such privacy measures from the outset can be a wise long-term strategy.

Integrating Protection with Long-Term Planning

Effective real estate asset protection isn’t a standalone endeavor; it’s an integral component of a broader, long-term financial strategy that includes estate planning and tax optimization. The goal is to create a cohesive plan that safeguards our assets, minimizes tax liabilities, and ensures a smooth transfer of wealth to future generations. For individuals considering various property types, such as Pahrump short sale homes, understanding how these elements intertwine is crucial.

Balancing Tax Efficiency and Liability

When structuring real estate ownership for asset protection, it’s crucial to consider the tax implications. Certain asset protection vehicles, while excellent for liability shielding, might impact tax benefits. For example, placing a primary residence directly into an LLC, while offering liability protection, could cause us to forfeit certain homestead exemptions or capital gains exclusions that are typically available to individual homeowners. Therefore, a careful balance must be struck.

Estate planning tools like revocable living trusts can offer both asset protection and significant tax advantages. They allow for the probate-free transfer of assets to heirs, avoiding potentially lengthy and costly court processes. Furthermore, assets held in a living trust may qualify for a “stepped-up basis” upon the owner’s death, meaning the tax basis of the asset is adjusted to its fair market value at the time of inheritance. This can significantly reduce capital gains taxes for heirs when they eventually sell the property. Homestead exemptions, where available, also play a crucial role in protecting a primary residence from creditors, often up to a certain value or even unlimited in some states. Integrating these considerations ensures that our protection strategies don’t inadvertently create new tax burdens or undermine our long-term wealth transfer goals.

When to Consult Professional Specialists

Given the complexity and state-specific variations of asset protection laws, attempting to navigate these waters alone can be risky. This is where the expertise of professional specialists becomes invaluable. We should consider consulting estate planners, asset protection attorneys, and experienced financial advisors when:

- Acquiring New Properties: Before making a significant real estate investment, especially for rental or commercial purposes, professional advice can help us choose the most appropriate ownership structure from the outset.

- Evaluating Current Holdings: If our real estate portfolio has grown or our personal financial situation has changed, it’s wise to have existing structures reviewed to ensure they still offer optimal protection.

- Facing Increased Risk: If we anticipate or are involved in a business venture that carries higher liability risks, or if our personal exposure to lawsuits increases, a specialist can help fortify our defenses.

- Planning for Succession: As part of broader estate planning, professionals can integrate asset protection strategies to ensure our legacy is preserved and transferred efficiently.

- Seeking Tax Optimization:Specialists can advise on how different protection structures impact our tax liabilities and help us balance protection with tax efficiency.

These professionals can conduct a thorough risk assessment, identify vulnerabilities, and design a customized, multi-layered asset protection plan that aligns with our specific financial goals and risk tolerance. Their expertise ensures that our strategies are legally sound, effective, and compliant with relevant state and federal regulations.

Frequently Asked Questions about Real Estate and Property Protection

How does an anonymous trust provide privacy?

An anonymous trust, often structured as a land trust, provides privacy by separating the legal ownership of a property from its beneficial ownership. When a property is placed into such a trust, the name of the trustee (an entity or individual appointed to manage the trust) is recorded on public records as the legal owner. Our identity, as the beneficiary who controls the property and receives its benefits, remains confidential and is not disclosed in public filings. This makes it difficult for potential litigants or curious parties to connect the property to our personal wealth or identity. If an LLC is also involved, the trust can own the LLC, further obscuring the beneficial owner’s identity from any public record notice associated with the property or the business entity.

What are the limitations of standard title insurance?

Standard title insurance primarily protects against defects in the title that existed before the property was purchased. Its main limitation is that it generally does not cover issues that arise after the closing, such as post-closing fraud (e.g., deed forgery that occurs years after purchase). Furthermore, standard title insurance policies, including enhanced ALTA (American Land Title Association) policies like the ALTA Homeowner’s Policy or ALTA 49 endorsement, often have exclusions for properties held by business entities like LLCs. This creates a significant coverage gap for real estate investors who use LLCs for liability protection, leaving their most vulnerable properties exposed to post-closing title fraud. This gap highlights the need for additional, proactive protection measures beyond traditional title insurance.

Why is equity stripping effective against lawsuits?

Equity stripping is effective against lawsuits because it reduces the perceived financial attractiveness of a property as a target. By encumbering a significant portion of a property’s value with debt (e.g., maintaining a 75% loan-to-value ratio), we reduce the accessible cash value that a plaintiff could seize if they win a judgment. If a property has limited equity that can be readily accessed, it becomes an “unattractive target” for lawsuits. Litigants and their attorneys often perform due diligence to assess the potential recovery from a lawsuit. If they see that a property is heavily mortgaged or has legitimate liens recorded against it, they may conclude that the legal costs and effort to pursue a claim against that property would outweigh the potential payout. This strategy, often involving recorded mortgages or other legitimate debt instruments, helps to shield the property’s underlying value from judgment liens.

Conclusion

Navigating the complex world of real estate ownership in May 2026 demands a sophisticated and proactive approach to asset protection. From the foundational use of LLCs and trusts to advanced financial tactics like equity stripping and the critical safeguard of comprehensive insurance, a multi-layered strategy is essential. We’ve explored how to defend against modern threats like deed fraud, emphasizing the need for active defense beyond traditional alerts. Integrating these protective measures with sound tax and estate planning ensures not only the security of our investments but also their efficient transfer to future generations.

The key takeaway is that comprehensive coverage and proactive structuring are not luxuries but necessities in today’s litigious and evolving real estate market. By understanding the risks and implementing the right strategies, we can significantly reduce our exposure and preserve our wealth. For those seeking to secure their real estate future, connecting with a local expert to explore secure investment opportunities is a prudent next step.

- Pantagonar: The Complete Guide to Smarter SEO and High-Quality Backlink Building

- Acamento: Everything You Need to Know About Modern Home Finishing

- Spaietacle: The Future of Smart Eyewear That Combines Style, Space, and Digital Innovation

- Insetprag: The Practical, Purpose-Driven Design and Integrated Systems

- PLG Supplies: The Smarter Supply Chain Management, Safety, and Business Efficiency